Verizon’s nationwide wireless outage on January 14, 2026, was the kind of event that doesn’t just disrupt a Tuesday: it hands every competitor field rep a talking point they’ll use for the next 18 months. Recon Analytics surveyed 1,702 business decision-makers between January 21 and February 25, 2026, capturing reactions in the immediate aftermath. The results tell a story that is both better and worse for Verizon than the company probably wants to hear.

The Outage Was Not Felt Equally

The January 14 outage was not a uniform experience across the business market. Impact scaled with company size, and the 23-percentage-point spread between large and small business is the first structural finding.

Large businesses reported the highest direct impact: 44% said the outage affected their company. Midsize companies came in at 33%. Small businesses sat at 21%. The remaining respondents in each segment indicated either no impact or were unsure. The gradient makes operational sense. Large organizations run more lines, more devices, more mission-critical workflows over wireless. A national field service operation or a distributed retail chain has thousands of points of exposure. A five-person shop has a handful. The outage hit large businesses hardest because they have the largest surface area. Large enterprises also operate more redundancy infrastructure, dedicated IT, secondary carrier contracts, Wi-Fi fallback. Whether the 44% figure reflects greater network dependency or greater issue-reporting sensitivity is not separable from this data.

The awareness data runs in the opposite direction. Among small businesses, 12% said they weren’t even aware an outage had occurred, compared to 3% of large enterprises and 7% of midsize. Small businesses run lean. If the phones worked well enough that day, or if the outage was brief enough in their geography, it didn’t register as a business event. Large enterprises have someone whose job is to know when the carrier goes down.

This awareness asymmetry matters for Verizon’s sales team. The enterprise segment felt the outage acutely and paid attention. That’s also the segment where Verizon has historically leaned on network reliability as its core value proposition. The pitch is that you pay more because the network doesn’t go down. January 14 complicated that pitch in the accounts where it matters most.

Figure 1: Was anyone in your company impacted by the Verizon Wireless outage of January 14th, 2026?

Source: Recon Analytics B2B Pulse, January 21st-February 25th, 2026. Percentages based on business respondents. Total n = 1,702, MoE = 2.4%; Large Business (1,000+ employees) n = 561, MoE = 4.1%; Midsize (20-999 employees) n = 538, MoE = 4.2%; Small Business (<20 employees) n = 603, MoE = 4.0%

Opinion Change Was Contained, Not Neutral

Among business customers who were aware of the outage, stated opinion change was limited. Across all size segments, roughly two-thirds said the outage did not change their opinion of Verizon. Opinion stability was statistically consistent regardless of company size.

The more operationally significant data is among those whose opinions did shift. Roughly 5-6% across segments said, “much more negative” and 27-29% said “somewhat more negative.” Combined negative sentiment ran approximately 32-35% across all segments. For an event that hit on a single day lasting about 10 hours, generating negative opinion change in roughly a third of aware business customers is a credibility problem if the narrative isn’t actively managed.

One caveat on the “no change” majority: it captures two distinct customer types that the data cannot separate. The first is the genuinely loyal customer who considers this within the bounds of acceptable carrier performance and has no intention of changing anything. The second is the customer who already held a neutral or negative opinion of Verizon before January 14, who are already at risk of leaving. Both sit in the same response bucket. The data cannot tell you how large each population is.

Figure 2: (only if impacted by outage) How has the network outage changed your opinion of Verizon Wireless?

Source: Recon Analytics B2B Pulse, January 21st-February 25th, 2026. Percentages based on business respondents who indicated they were impacted by the outage. Total n = 551, MoE = 4.2%; Large Business n = 246, MoE = 6.2%; Midsize n = 179, MoE = 7.3%; Small Business n = 126, MoE = 8.7%

The Loyalty Question Is Where the Size Gap Becomes a Revenue Conversation

Because no pre-outage baseline is available for switching intent in this sample, the figures below represent a post-event snapshot, not a measured change from prior intent levels.

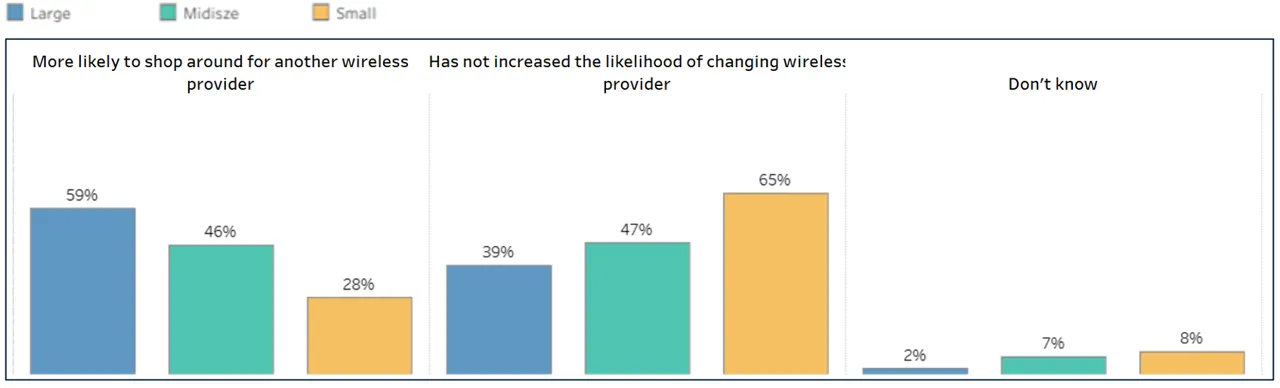

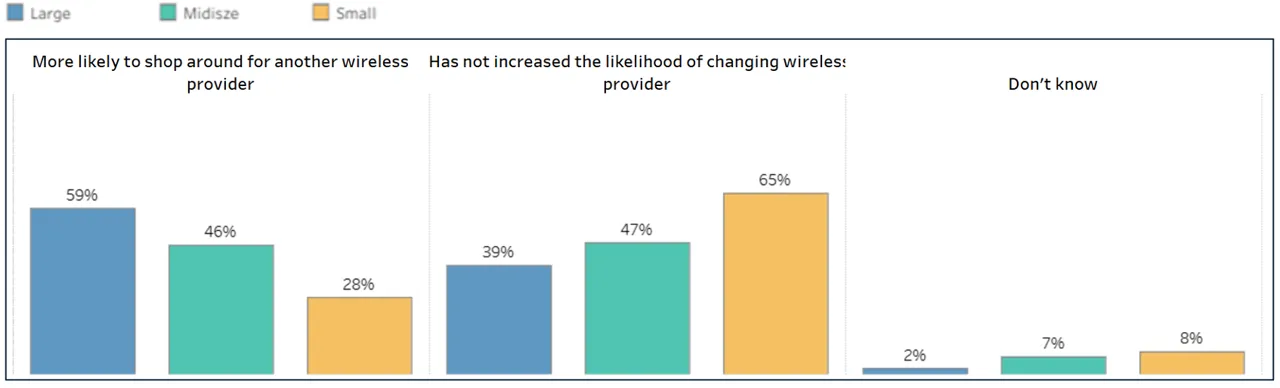

Among current Verizon Wireless business customers asked how the outage affected their likelihood of staying after their current agreement, small businesses were the most forgiving: 65% said the outage had not increased their likelihood of changing providers, 28% said they were more likely to shop around, and 7% were unsure or did not respond. Large businesses showed a different picture, with 39% saying the outage had not increased their likelihood of switching, 59% said they were more likely to evaluate alternatives, and 2% were unsure. Midsize was a statistical tie.

Among large business Verizon customers, 59% said the January 14 outage made them more likely to evaluate alternatives when their contract comes up. Remember, intent to shop is different from switching. Contract lock-in, device payoff schedules, multi-line complexity, and the operational headache of migrating a large business all create meaningful friction between stated intent and revealed behavior. Enterprise switching intent historically overstates eventual switching behavior. Even accounting for that gap, a post-event snapshot where 59% of large business Verizon customers express elevated interest in alternatives is a leading indicator that the competitive pipeline has expanded.

Enterprise wireless agreements typically run one to three years. The cohort of large accounts whose contracts expire in 2026 and 2027 is now at elevated churn risk compared to January 13. Verizon’s enterprise sales team should be in front of those accounts before AT&T and T-Mobile arrive with a pitch deck that opens on January 14.

Figure 3: (currently using Verizon) How did the outage impact the likelihood of you staying with Verizon Wireless at your next renewal?

Source: Recon Analytics B2B Pulse, January 21st-February 25th, 2026. Percentages based on business respondents who self-reported current Verizon Wireless use. Total n = 510, MoE = 4.3%; Large Business n = 201, MoE = 6.9%; Midsize n = 167, MoE = 7.6%; Small Business n = 142, MoE = 8.2%

The Non-Verizon Market: Enterprise Forgives, Small Business Does Not

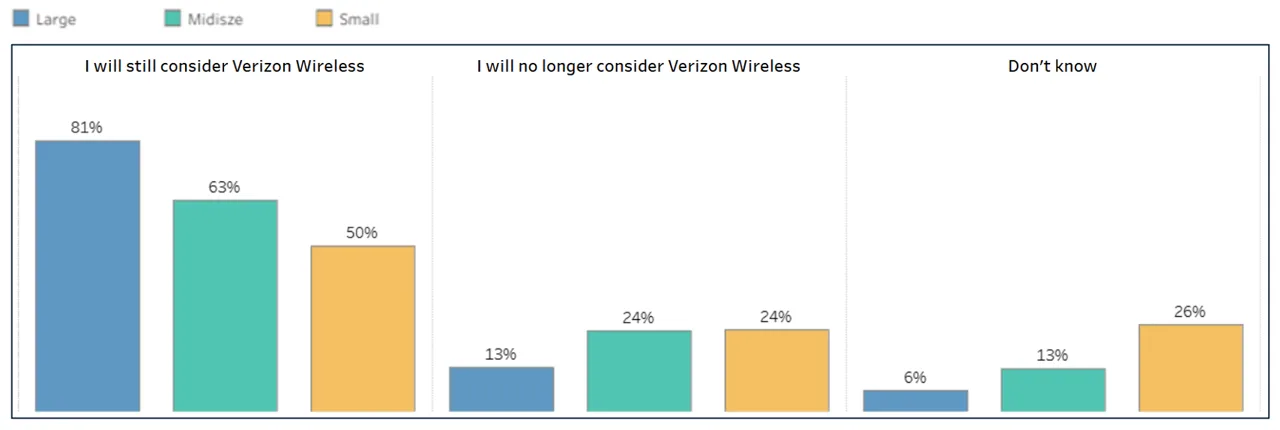

Among business customers not currently on Verizon, the outage produced differentiated responses that also track with company size.

Large businesses remained the most open to Verizon despite the outage: 81% said they would still consider Verizon when their current agreement expires. One bad day doesn’t remove a major carrier from consideration. Enterprise procurement decisions involve pricing, coverage, device ecosystems, and account support infrastructure. Small businesses reacted more negatively to the outage, even though they did not experience the outage directly. 24% of small businesses said they would no longer consider Verizon, while 26% said they were unsure. A single outage is a data point, not a disqualifier, but can unbalance customers that are on the fence.

Figure 4: (Not currently using Verizon) How did the outage impact the likelihood of you considering Verizon Wireless next?

Source: Recon Analytics B2B Pulse, January 21st-February 25th, 2026. Percentages based on business respondents who do not use Verizon Wireless (self-reported). Total n = 1,064, MoE = 3.0%; Large Business n = 341, MoE = 5.3%; Midsize n = 334, MoE = 5.4%; Small Business n = 389, MoE = 5.0%

What Verizon Has to Do Now

The January 14 outage created a two-front problem. In the existing base, large business accounts are at elevated renewal risk. In the prospect market, small businesses have partially written Verizon off. But both are addressable.

Verizon’s enterprise team should prioritize proactive outreach to its large account base before those contracts expire. Generic reliability commitments won’t land. The message needs to be specific: what failed, what was fixed, what redundancy was added, what the SLA improvement looks like going forward. Enterprises don’t need apologies. They need engineering answers.

On the prospect side, the small business perception problem is harder because it’s driven partly by information Verizon doesn’t control. The counter-narrative has to reach small business decision-makers through channels they trust: peer networks, trade media, and the resellers and agents who carry Verizon’s products into that segment.

The January 14 outage was one bad day, which must be addressed with customers to protect accounts that could take years to win back if lost.