ANALYSIS | US SMARTPHONE MARKET

The US smartphone market loves good narratives. Apple versus Samsung. Premium versus value. Loyal fans versus deal-hungry switchers. A new deep dive from Recon Analytics, based on 104,408 US consumers tracked over five quarters, is here to complicate every one of those stories.

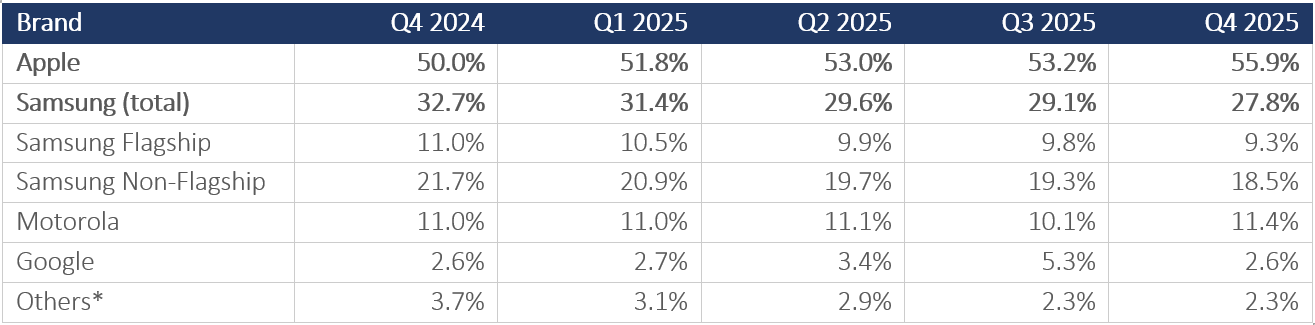

The headline is blunt: Apple ended 2025 with 55.9 percent of the US installed base, up 5.9 points in a single year. Samsung fell 4.9 points to 27.8 percent. The gap between the two brands, 28.1 points, is now 62 percent wider than it was twelve months ago. Five consecutive quarters of directional movement, with share gains accelerating rather than moderating, is consistent with a structural realignment rather than a cyclical fluctuation. The 2026 upgrade data will be the definitive test. The market share here is the installed base of over 104,000 US consumers, whose device information was passively collected during the survey. While we believe the data is robust, with a 0.3% margin of error (95% CI), the market share may still differ from the traditional shipments-based market share. The quarterly market-share trends based on the installed base provide a more directional analysis of the market than an absolute one.

Table 1.1: Quarterly Market Share Trends (% of Installed Base)

Note: *Others include OnePlus, LG, TCL, Xiaomi, Nokia, BLU, and remaining brands. Source: Recon Analytics US Mobile Device Components survey, Q4 2024–Q4 2025.

Note: *Others include OnePlus, LG, TCL, Xiaomi, Nokia, BLU, and remaining brands. Source: Recon Analytics US Mobile Device Components survey, Q4 2024–Q4 2025.

The Ecosystem Trap Nobody Can Escape

Apple is not winning on specs. The iPhone 17 series ships with a smaller battery than leading Android rivals. Its camera array does not top the industry benchmarks. What Apple has built instead is a gravitational field: iMessage, AirDrop, FaceTime, and the seamless handoff between iPhone, iPad, Mac, and Watch. Switching away from Apple does not just mean buying a new phone; it means abandoning a digital life. No hardware specification can compete against that.

The data confirms what Apple’s own marketing has long implied: its best salesperson is a current iPhone user. Friends and family recommendations ranked as the top research source for Apple buyers every single month across the May–December 2025 tracking period. No paid media budget can replicate a word-of-mouth engine that runs entirely within an installed base of 150 million-plus American consumers.

Samsung’s Two-Brand Problem

Here is the part of the Samsung story that most competitive analyses get wrong: there is no single Samsung. There are two, and blending them together produces numbers that are wrong for both.

Samsung Flagship, the Galaxy S, Z Fold, and Z Flip series, averaged $1,056 per device in Q4 2025 (Recon Analytics US Mobile Device Components survey, Q4 2024 – Q5 2025). That is $69 above Apple’s average of $987. Samsung’s premium users are paying more than iPhone users. The Galaxy S and Ultra command high customer satisfaction, with a flagship satisfaction score (cNPS) of 32.4 (n=37,302, May-Dec 2025), compared to Apple’s 30.4 (n=107,406, May-Dec 2025). Note: the 2.0-point gap between these scores sits at the cNPS noise threshold; confirm subgroup-level margin of error before asserting a directional lead. The component net promoter score (cNPS) is Recon Analytics’ proprietary version of the NPS. Recon Analytics’ cNPS covers smartphones from 22 dimensions. Also, 64.4 percent of the Samsung flagship installed base is now in the 2-plus-year upgrade-eligible window. That is the most financially concentrated upgrade opportunity in Android heading into 2026.

Then there is Samsung Non-Flagship, the Galaxy A-series, averaging $243 per device in Q4 2025, down sharply from $316 a year ago (Recon Analytics US Mobile Device Components survey, Q4 2024–Q4 2025). Its satisfaction score (cNPS) sits at 22.3, with 26.9 percent of users actively detracting from the brand. The A-series does not just underperform; it creates potential brand-perception drag that shadows every Samsung consumer evaluation. The $813 gap between Samsung’s two tiers is the starkest within-brand pricing divide in the market.

The consideration data makes the structural problem concrete. Samsung Non-Flagship buyers cross-shop Apple at a higher rate than Samsung Flagship buyers, 23.1 percent versus 20.5 percent (Recon Analytics US Mobile Device Components survey, May-Dec 2025; Samsung Non-Flagship, n= 32,263, and Flagship n=37,302 respectively), and that gap widened through the second half of 2025. Whether this reflects an aspirational pull toward Apple specifically or the generally higher brand fluidity among value-tier buyers is a distinction the consideration data raises but does not fully resolve; both mechanisms likely contribute.

Google Ran an Experiment. The Results Were Not Encouraging.

Google’s 2025 is a case study in the difference between rented share and owned share. Pixel climbed from 2.6 percent of the US installed base in Q4 2024 to 5.3 percent in Q3 2025, driven by carrier promotions and the launch of the Pixel 10. By Q4 2025, it was back at exactly 2.6 percent. Exactly where it started. The precision of that reversion is striking.

The hardware was not the problem. Google Pixel Pro earned the highest device-level satisfaction score (cNPS) in the entire dataset, 33.2 cNPS, with the lowest detractor rate among all flagship-tier devices. The product genuinely converts buyers into advocates. The challenge is that Pixel advocacy operates largely outside the physical environment where most purchase decisions are finalized. Pixel devices appear on carrier websites, but are underrepresented in the physical store, according to Recon Analytics’ survey data (see upcoming Consumer Device Purchase Journey – Part 3 report), 53 to 55 percent of US device sales through carrier and big-box channels are driven by in-store staff recommendations, floor placement, and promotional subsidies — not web listings. A phone can be available online and still be invisible at the point of conversion. That is Google’s distribution problem: not absence from the catalog, but absence from the moment that matters.

Google’s 2025 trajectory is the reference point every brand strategist in this market should keep close to. A promotion without a plan for what happens when it ends is a subsidy, not a growth strategy.

Motorola Does Not Get Enough Credit

While the industry fixates on the premium tier, Motorola has quietly done something harder than it looks: hold ground. The brand maintained 11.0 to 11.4 percent share across all five tracked quarters, with a consistent Q4 seasonal lift driven by holiday gift purchases. Its average device price runs around $313 to $333, flat across the year, with no pretensions toward premiumization. Motorola’s franchise is built on carrier placement and price discipline, and it executes that positioning with a consistency that belies its unglamorous reputation.

The satisfaction picture is mixed: non-flagship CNPS at 20.7 (cNPS), with 28.6 percent detractors, suggests elevated hardware quality friction at the low end, but the brand’s structural stability in a year when Samsung shed nearly 5 points is nothing.

The Upgrade Pipeline That Will Define 2026

Here is the question that makes 2025’s data genuinely consequential: what happens to the upgrade cycle next year?

Apple’s 51.9 percent upgrade-eligible rate, applied to its dominant installed base, produces the largest absolute pool of upgrade-ready consumers in the market. Samsung Flagship’s 64.4 percent eligible rate, though applied to a smaller base, represents the single most financially concentrated upgrade opportunity in Android. The two pools together define the 2026 replacement market.

Samsung’s most immediate strategic decision is whether it converts that aging flagship base before Apple does. Galaxy S users are holding devices longer than any other tracked segment and are currently cross-shopping Pixel as their primary Android reference point rather than iPhone. That is a narrower competitive window than most Samsung strategists probably assume. If Samsung can capture the upgrade cycle with its own flagship base, the share-loss story changes. If Apple absorbs another wave of premium converts, the 28-point gap could widen further.

The data does not predict outcomes. But it tells you exactly where the pressure points are, which side has the momentum, and which brand’s growth is real. Right now, Apple has the momentum. Google has the product but not the shelf. Samsung has two businesses that need two strategies. And Motorola has quietly survived a year that was much rougher than the headline numbers suggest.

The 2026 upgrade cycle is loaded. Whoever takes it may well determine whether this is a structural realignment or a temporary gap. The thesis that this is a structural shift, not a cycle, has three observable tests. First: if Samsung Galaxy S26 captures more than 55 percent of its own upgrade-eligible base in Q1-Q2 2026, the share-loss momentum is arrestable. Second: if Apple’s installed base reaches 58 percent by Q2 2026, the shift is accelerating past Samsung’s realistic recovery window. Third: if Google’s share holds above 3.5 percent through Q2 2026 without a promotional event, it has converted rented share into owned share for the first time. Any one of these outcomes materially changes the 2026 forecast.

Note: This analysis covers the US smartphone installed base from Q4 2024 through Q4 2025. It does not address global market dynamics where Samsung’s competitive position differs materially; carrier incentive structures that drive short-term share movements independent of brand preference; or price elasticity effects that may account for some portion of Apple’s installed base growth. These variables are available for analysis in subsequent phases of the device-purchase-journey study. If you want to find out more about the Recon Analytics’ US Consumer Device Purchase Journey Part 1: Market Landscape, Brand Performance & Consumer Satisfaction report, which is based on 104,408 US respondents tracked from Q4 2024 through Q4 2025, please visit here: US Consumer Device Purchase Journey – Part 1: Market Landscape, Brand Performance & Consumer Satisfaction – Digital Product Reports