May 2026

Satellite internet used to mean one thing in the business world: a slow, expensive connection of last resort when nothing else was available. HughesNet and Viasat filled that role for years, and nobody was excited about it. LEO satellite operators, including Starlink, have changed that story. Lower latency, faster speeds, and a product that can actually compete with fixed wireless have moved satellite from the back of the options list to a legitimate part of businesses’ connectivity fabric. However, even with greater acceptance of LEO satellite communications, Starlink still has a limited market position.

The Coverage Gap Story

The strongest direct sales case for Starlink in business markets is the coverage gap. Go where the competition does not. It sounds simple, and in a lot of ways it is.

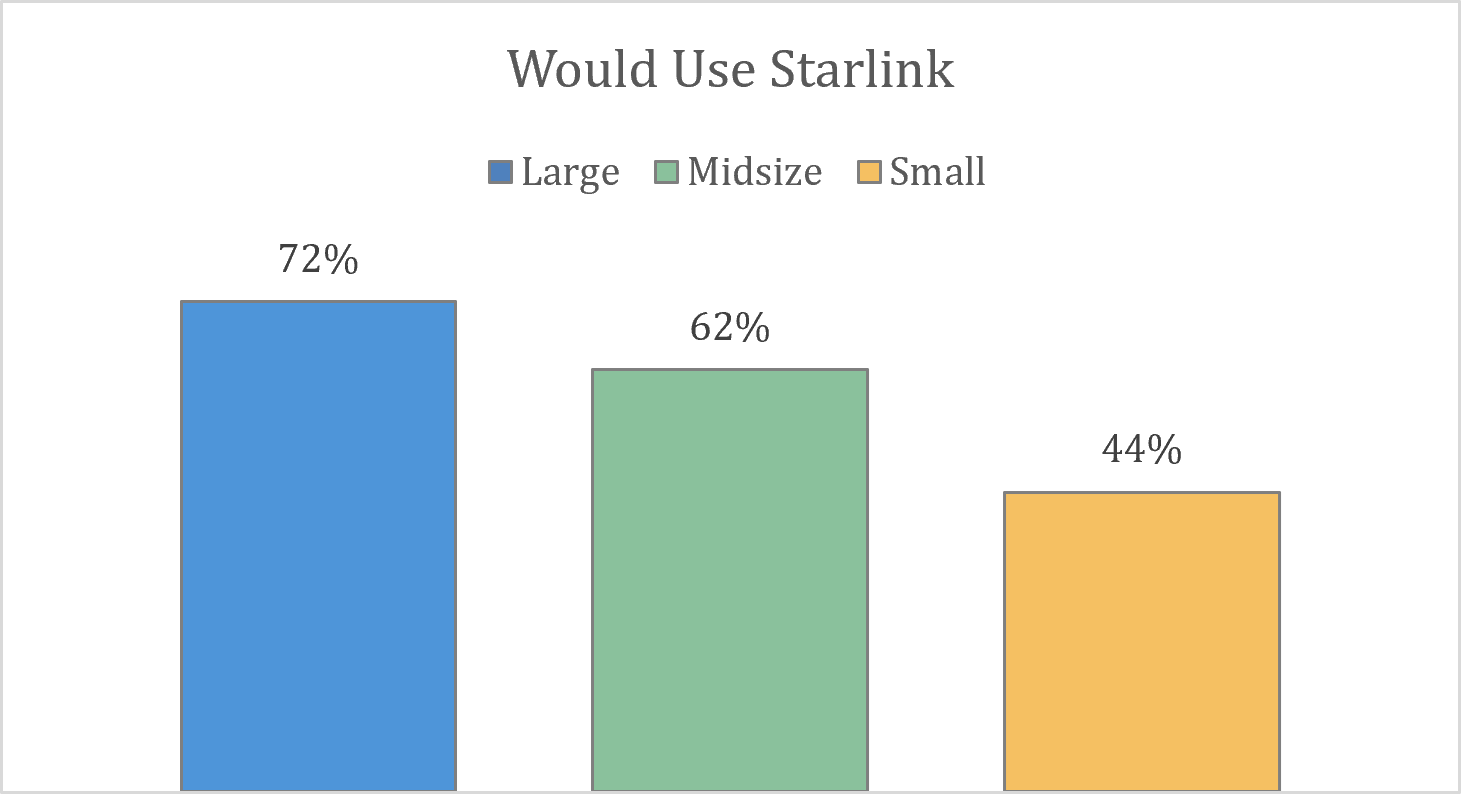

Between March 4 and April 7, 2026, we asked businesses whether they would work with a smaller ISP if that ISP could deliver Starlink connectivity in places where they currently had no coverage (Large n=586, Midsize n=455, Small n=554). Large businesses came in at 72%, midsize at 62%, and small businesses at 44%. The 28-point spread between large and small is the part worth paying attention to. Large businesses are most receptive because they are most likely to already be living with this problem. A company with 50 locations almost certainly has some of those locations sitting outside fiber and cable reach. A small business with one rural location either has the problem or it does not. For the large enterprise managing a dispersed footprint, a Starlink-augmented ISP solves something concrete and immediate.

Figure 1. Percent of Respondents Who Would Work with a Smaller ISP if They Augmented Coverage with Starlink

Source: Recon Analytics 3/4/2026-4/7/2026, Large n = 586, Midsize n = 455, Small n = 554

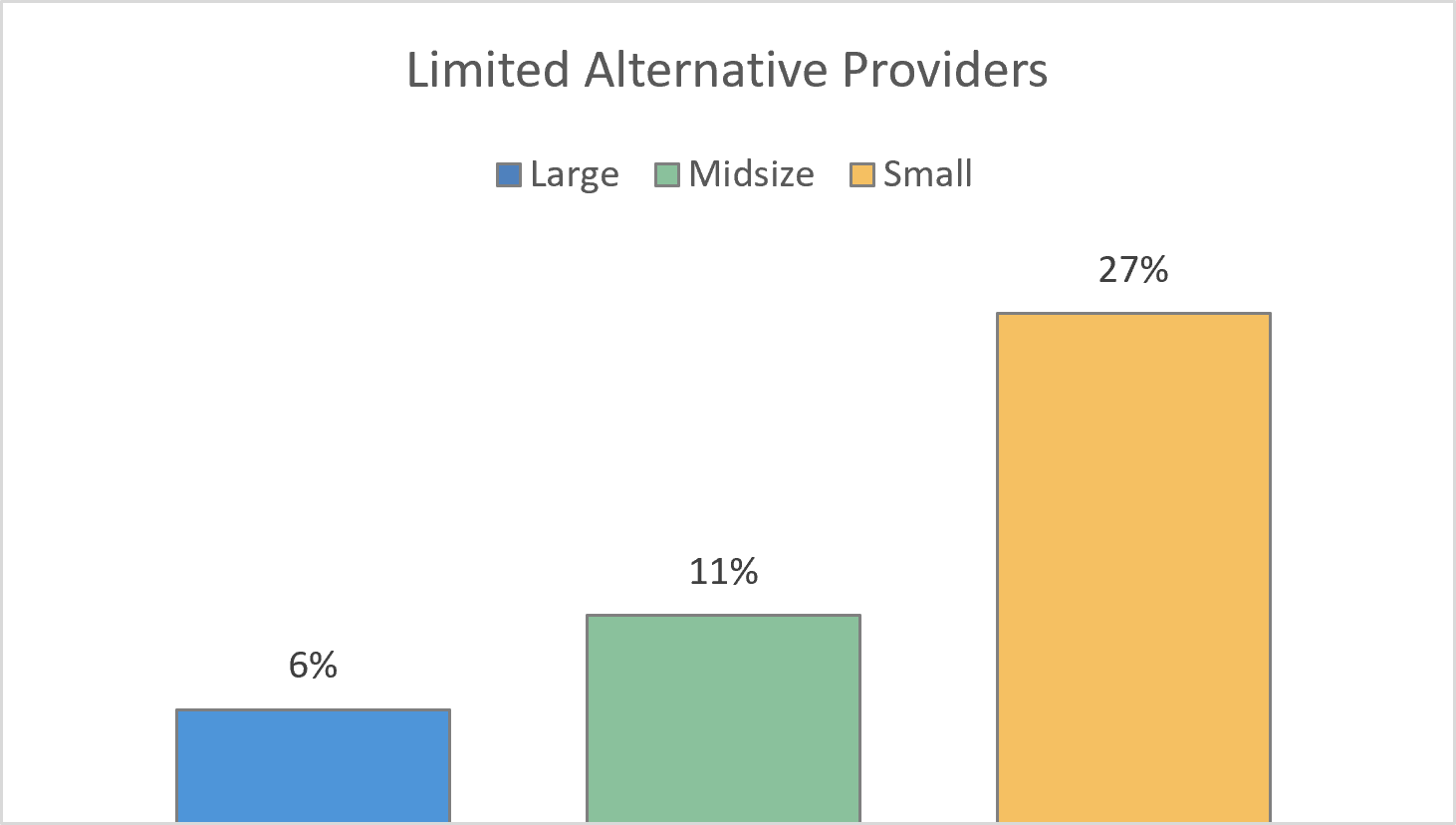

The second piece of data that helps to illustrate the coverage gap opportunity for Starlink comes from a different question. Between November 5, 2025, and May 6, 2026, we surveyed 9,913 businesses and found 1,483 that were unhappy with their current internet provider but had not switched. Among small businesses in that group, 27% said the reason they had not left was simple: there were no other options. For midsize businesses it was 11%, and for large businesses just 6%.

That 27% small-business figure is where Starlink’s direct-sales pitch is at its strongest. When a business is stuck with a provider they dislike because there is literally nothing else, Starlink is not going head to head with a well-resourced competitor. It is filling a gap that nobody else is filling. That is a very different conversation.

Figure 2. Limited Alternative Internet Provider as Reason to Stay with Current Provider

Source: Recon Analytics 11/5/2025-5/6/2026, Large n = 361, Midsize n = 502, Small n = 620

Moving outside of areas with little to no broadband access will be more difficult for Starlink as larger businesses do not just buy connectivity from their ISPs. Larger businesses buy a full suite of solutions including security, direct cloud connectivity, and SD-WAN. These are all services that Starlink does not provide. Starlink, currently, just provides connectivity.

The FWA Backup Case

The satellite-as-backup to primary internet access is Starlink’s other major business connectivity opportunity. Starlink does not need to win the primary internet relationship here. It just needs to be there when the primary connection goes down.

AT&T and Verizon already do something similar with FWA. Both service providers use their FWA network as a failover solution incase the primary internet access line they provide should have an outage. Satellite can provide the same function in areas where FWA is not available or where FWA is the primary access technology.

Recon Analytics tested this concept directly with U.S. businesses during the first half of 2026. Between April 1 and April 29, 2026, we asked businesses whether satellite backup would make FWA a more attractive primary connection (Large n=525, Midsize n=464, Small n=563). Large and midsize businesses both came in at 34%. Small businesses were at 24%. These numbers predate T-Mobile’s SuperBroadband announcement in May 2026, which matters. Starlink failover is one of key features of SuperBroadband. This is demand that existed before the product launched, not demand manufactured by a marketing push.

The practical reality, though, is that the FWA backup opportunity mostly runs through carriers, not through Starlink’s direct sales team. T-Mobile owns the customer relationship in SuperBroadband. Comcast Business owns it in its managed connectivity offering which utilizes Starlink as well. That is a lower-margin model than selling direct, and it means accepting a role as infrastructure provider rather than service provider. The upside is scale. Carrier channels can reach enterprise accounts and multi-location businesses that Starlink cannot do as efficiently on its own.

The longer-term question for Starlink is whether it stays in that infrastructure role or eventually moves to compete directly in markets where carrier partners currently hold the customer. Nothing in Starlink’s commercial agreements with T-Mobile or Comcast prevents it from doing so. The constraint right now is product fit, not contract language. That distinction is worth keeping in mind when thinking about how durable these partnerships really are. The recently announced joint venture between AT&T, T-Mobile, and Verizon on direct-to-device satellite communications could complicate Starlink’s relationship with T-Mobile and be a catalyst for Starlink to take a more aggressive role in selling directly to businesses.